As MRP noted back in April, a new wave of mergers and acquisitions (M&A) in biotech and pharma could be on the horizon. Jefferies analyst Michael Yee estimates that the combined market capitalization of all the biotech stocks valued at under $5 billion is around $350 billion. That compares to a combined cash balance among the top 20 biopharma companies worth over $300 billion. “We have reached a point where Big Pharma has so much cash they could basically buy the whole smid-cap universe,” Yee wrote.

At the end of last year, MRP highlighted a report from SVB Leerink analyst Geoffrey Porges and his team, estimating that eighteen large-cap US and European biopharmas will have more than $500 billion in cash on hand by the end of 2022. Porges said those 18 biopharma majors will have total M&A capacity of $1.72 trillion.

Wells Fargo analysts have echoed that assessment of cash balances among major pharmaceutical and biopharma firms. In a recent note, cited by VettaFi, the analysts wrote “Big BioPharma needs growth, and the 5 major US companies with the biggest need have $400B+ cash available from now to 2025, and revenue need of ~$65B+.”

There have been a couple of false starts to an expected surge in dealmaking thus far. In particular, Pfizer Inc’s $11.6 billion deal for migraine specialist Biohaven Pharmaceutical in April, marking the biggest deal in the biopharma space so far this year, as well as GlaxoSmithKline’s dual acquisitions of cancer-focused Sierra Oncology, Inc. and clinical-stage vaccine developer Affinivax for $1.9 billion and $3.3 billion, respectively.

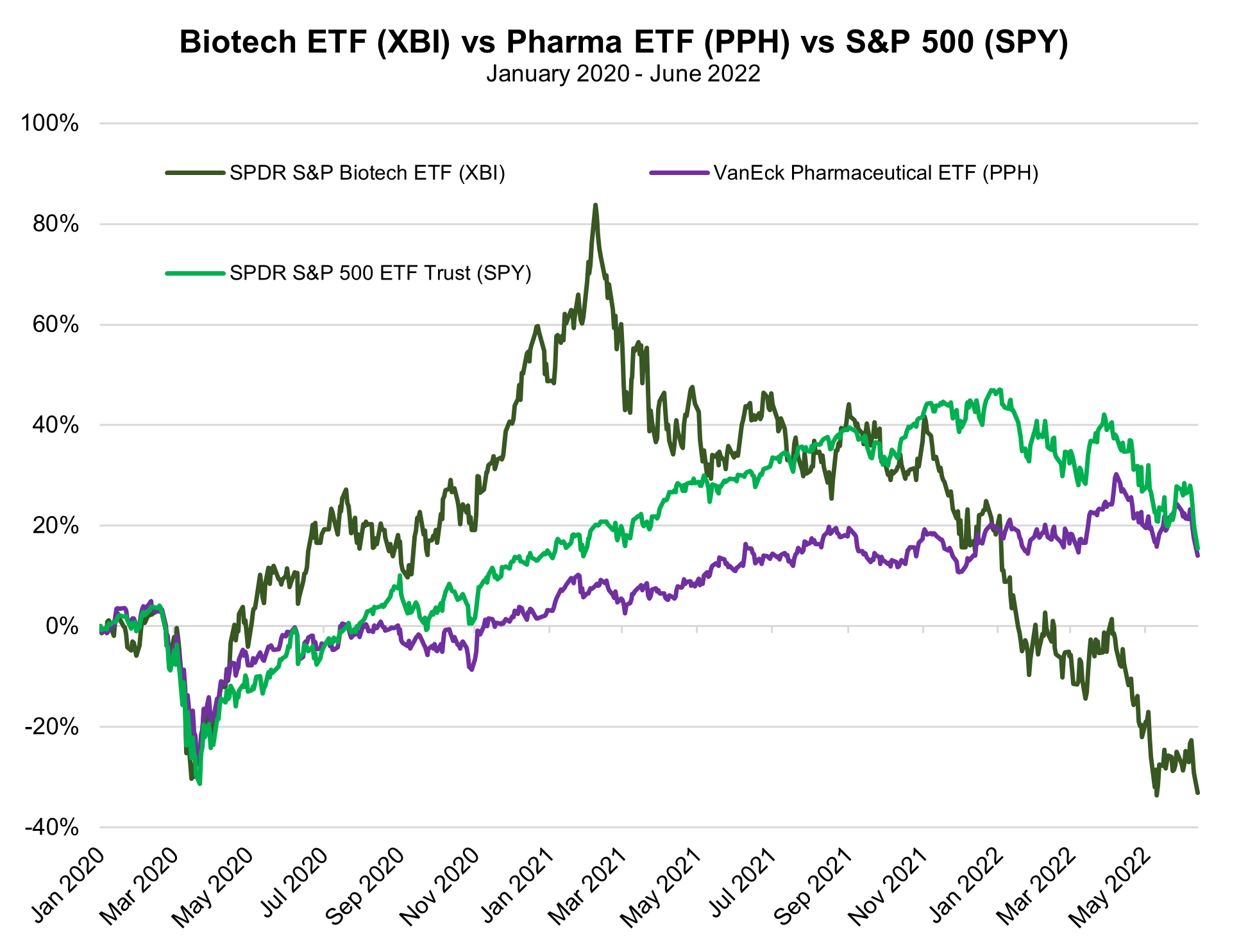

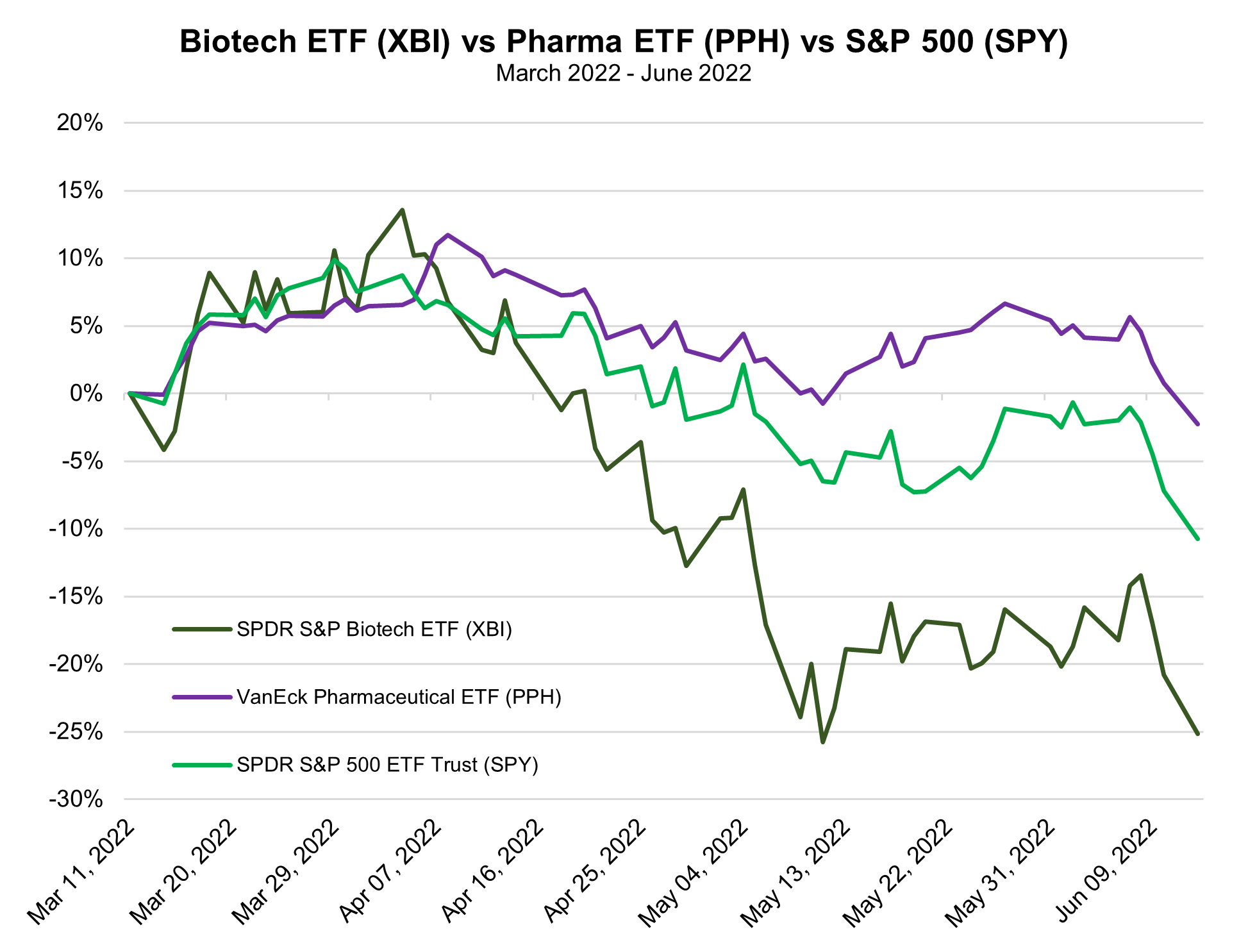

While those deals have been significant, most biopharma giants have been open about their desire for even lower prices before they begin deploying their massive cash reserves. Per a CB Insights report, cited by Fierce Biotech, there was a 60% drop in M&A exits in the first quarter, with just six recorded, compared to 15 in the fourth quarter of 2021. The hesitance is not extremely surprising, given a continually aggressive sell-off in publicly traded biotech firms, as well as mass layoffs throughout all ranks of firms in the space.

The souring state of public and private markets continues to water down the potential for VC raises and IPOs, as well as other funding methods like Special Purpose Acquisition Companies (SPACs).

Per Crunchbase News, biotech startups have raised a total of $16.5 billion so far this year in the US, or about $3.2 billion on average per month. In all of 2021, however, nearly $47 billion went into the space, an average of nearly $4 billion per month. Meanwhile, the IPO pipeline remains mostly shut off. Crunchbase data identifies just nine VC-funded biotech IPOs this year.

A dearth of deals has been especially rough on SPACs.

As TechCrunch recently wrote, many SPACs, also known as blank-check companies, now must find suitable targets in a market turned bearish, and the clock is ticking. Given that blank-check companies are typically expected to merge with a target company within 24 months of investors funding the SPAC, if those hundreds of SPACs can’t complete mergers with candidate companies within the first half of next year, they’ll either have to wind down (which can means millions of lost dollars for SPAC sponsors) or else seek out shareholder approval for extensions.

Between the middle of 2021 and February 2022, at least 22 were called off, according to Bloomberg and data compiled by Chicago-based SPAC Research. Toward the end of that span, biotech firm Amicus Therapeutics’ SPAC deal with ARYA Sciences Acquisition Corp IV unraveled, costing the company about $400 million, along with its plans to achieve profitability by 2023 and potential clinical testing for several gene therapies.

As Fierce Biotech reports, one of the latest SPACs to be spiked was Blade Therapeutics, which set out plans for a blank-check deal in November 2021 with SPRIM Global Investments' special purpose acquisition company that would have given Blade about $255 million to bankroll trials in fibrosis and neurodegenerative conditions. This downturn in SPAC deals continues to deal significant blows to biotechnological research and slow the pace of development in the pipeline.

Some SPACs are beginning to get creative to avoid extensions or losses and biotech may be leading the way in saving some 600 SPACs that are still out there hunting for deals before their respective deadlines. Per CNBC, Bull Horn Holdings has decided to merge with biotech Coeptis Therapeutics, a public company traded over the counter – bucking the traditional SPAC model of taking private companies into public markets. |